|

|

"Heck's Coming With Me"

Posts: 10797

Location: Kansas | You know how for 2016 the administration decided recipients didn't need a raise in Social Security, even though many senior citizens totally depend on it. Well, for 2017 the raise will be.. (drumroll).. two-tenths of one percent, or about $3 per recipient. Why bother? The real kick in the teeth is when I see illegals interviewed on TV counting their numerous blessings from U.S. taxpayers and including Social Security in the mix.

| |

| | |

| AMERICANS FIRST ......... VOTE FOR DONALD J. TRUMP!! | |

| | |

To the Left

Posts: 1865

Location: Florida | I have money in a savings account and I make one tenth of one percent interest. The people getting screwed are the people who save money and get nothing because the Feds keep the interest rate at nothing to help businesses loan our money at an 18% profit. | |

| | |

Semper Fi

Location: North Texas | Vickie - 2016-06-24 2:00 PM

I have money in a savings account and I make one tenth of one percent interest. The people getting screwed are the people who save money and get nothing because the Feds keep the interest rate at nothing to help businesses loan our money at an 18% profit.

Want to see a economy completely grind to a halt? Raise the interest rates! History tells that high interest rates i.e. Carter Administration have long lasting consequences! Twas the mid to late '80s before the economy actually recovered from high interest rates!

| |

| | |

Location: Not Where I Want to Be | Vickie - 2016-06-24 3:00 PM I have money in a savings account and I make one tenth of one percent interest. The people getting screwed are the people who save money and get nothing because the Feds keep the interest rate at nothing to help businesses loan our money at an 18% profit.

I know I should never bite on your fishing expeditions.

But that statement is one of the more insanely idiotic claims that I may have ever read on this site.

Savings accounts are not investment vehicles. You want you money to work for you, put it to work. Don't stash it.

| |

| | |

Own It and Move On

Location: The edge of no where | 1DSoon - 2016-06-24 2:06 PM Vickie - 2016-06-24 3:00 PM I have money in a savings account and I make one tenth of one percent interest. The people getting screwed are the people who save money and get nothing because the Feds keep the interest rate at nothing to help businesses loan our money at an 18% profit. I know I should never bite on your fishing expeditions.

But that statement is one of the more insanely idiotic claims that I may have ever read on this site.

Savings accounts are not investment vehicles. You want you money to work for you, put it to work. Don't stash it.

^^THANK YOU | |

| | |

Take a Picture

Posts: 12841

| 1DSoon - 2016-06-24 2:06 PM

Vickie - 2016-06-24 3:00 PM I have money in a savings account and I make one tenth of one percent interest. The people getting screwed are the people who save money and get nothing because the Feds keep the interest rate at nothing to help businesses loan our money at an 18% profit.

I know I should never bite on your fishing expeditions.

But that statement is one of the more insanely idiotic claims that I may have ever read on this site.

Savings accounts are not investment vehicles. You want you money to work for you, put it to work. Don't stash it.

That was pretty much what I was thinking. I think I have a better interest rate on my checking account than that | |

| | |

"Heck's Coming With Me"

Posts: 10797

Location: Kansas | MS2011 - 2016-06-24 2:12 PM

1DSoon - 2016-06-24 2:06 PM Vickie - 2016-06-24 3:00 PM I have money in a savings account and I make one tenth of one percent interest. The people getting screwed are the people who save money and get nothing because the Feds keep the interest rate at nothing to help businesses loan our money at an 18% profit. I know I should never bite on your fishing expeditions.

But that statement is one of the more insanely idiotic claims that I may have ever read on this site.

Savings accounts are not investment vehicles. You want you money to work for you, put it to work. Don't stash it.

The stock market is and always will be volatile.......not always a good idea for senior citizens.

| |

| | |

"Heck's Coming With Me"

Posts: 10797

Location: Kansas | foundation horse - 2016-06-24 2:03 PM Vickie - 2016-06-24 2:00 PM I have money in a savings account and I make one tenth of one percent interest. The people getting screwed are the people who save money and get nothing because the Feds keep the interest rate at nothing to help businesses loan our money at an 18% profit. Want to see a economy completely grind to a halt? Raise the interest rates! History tells that high interest rates i.e. Carter Administration have long lasting consequences! Twas the mid to late '80s before the economy actually recovered from high interest rates!

You're talking about extraordinarily high interest rates.....not the normal 5 or 6 percent.

| |

| | |

Regular

Posts: 94

Location: Texas | Social security was always mean to "help supplement seniors" not be the sole source of support/income!!

Don't depend on someone else to take care of you! Do what you can now to make sure that your retirement is secure! | |

| | |

Semper Fi

Location: North Texas | prober - 2016-06-25 6:00 AM

Social security was always mean to "help supplement seniors" not be the sole source of support/income!!

Don't depend on someone else to take care of you! Do what you can now to make sure that your retirement is secure!

In reality, it is NOT The Government's Job to take care of anyone, period!

Social Security was pitched by FDR, an American Progressive/Socialist as The Government Retirement Plan, which Congress as since absconded with via depositing SS receipts in The General Fund vs. The Private Fund which SS was originally designated to be held in.

So, in reality The Federal Government is screwing it's Citizens..............Again!

| |

| | |

BHW Resident Surgeon

Posts: 25352

Location: Bastrop, Texas | Don't get me started on Social Security. There's no earthly reason why the program should continue indefinitely. I'm waiting for a courageous politician to come out and put forth a sensible argument in favor of transitioning to a privatized system.

As 1D Soon suggested, if you want to save for retirement, the best way to accomplish that is to put your money where it will work for you and grow. Allowing the fed government to confiscate it from you for your entire life won't get you there. Social Security is just as bad as a Ponzi scheme. Bank savings accounts are not money gardens, and the federal government is even worse. Politicians for decades have used criminal scare tactics to convince the unthinking that privatization is somehow dangerous. No matter where you put your money, there will always be risk. At the top of the list of lousy vehicles, in terms of investing for retirement, is social security. It's already failing.

Consider this scenario. If you start contributing 12.4% of your income at age 20 to retirement, you retire at age 60, and you average an annual income of $40K per year, assuming an average annual rate of growth of 7% over those 40 years, how much would your nest egg be worth? Answer: about $1.2 Million. Don't believe me? Figure it out for yourself. Go back and look up the average rate of growth of equities over the last 100 years. If you start with the stock market crash of 1929 until present day, the average rate of growth in the market is roughly 8.5%. If you start in 1932, when the economy started to recover, the rate of growth was roughly 11%. I used a very conservative 7% figure. If I used that 11% figure, then in the above scenario, your nest egg would be worth about $3.5 million. Let's assume the less optimistic scenario of 7% - that means if you draw 5% off that nest egg to live on, your retirement income would be $60K per year for the rest of your life.....when you were used to living on much less during your working years. Your nest egg probably wouldn't change much through your retirement. That would remain as your "money tree" which could be passed on in your estate when you pass away. If you die before reaching retirement, the government can tear up that IOU, if you have no dependents. In a privatized system, it goes wherever you designate.

Here's another huge, albeit less appreciated, advantage of privatization. All that money in privatized retirement would amount to an annual infusion into the economy. We're talking about hundreds and hundreds of billions of "stimulus" dollars into the private sector. That's REAL money, not borrowed money like the 2009 stimulus bill. That creates jobs. But here's another beautiful bonus, for those of you fearing that the government would be left out: all that money and those jobs generate incomes, and hence tax revenues to the fed. You want to eliminate the federal debt? Privatize social security! You want to be able to afford to provide some aid to indigents WITHOUT borrowing money or raising taxes? Privatize social security! You want to provide INCENTIVE to work? Privatize social security and it won't be long before even lazy people realize that they want in on the game.

Of course maybe that is "too risky". Maybe it's too good to be true.

Well, that's what our elected officials tell us anyway. After all, they are so much smarter than the rest of us........aren't they? | |

| | |

Member

Posts: 23

| Bear....this is the most common sense thing I've read in a long time. Sadly, no politician will have the balls to touch SS. | |

| | |

"Heck's Coming With Me"

Posts: 10797

Location: Kansas | Bear, when you talk about privatization, does that still stem from money the Govt took from your paycheck or a voluntary program, because most people would just simply spend the money. It would never go into savings.

| |

| | |

Shelter Dog Lover

Posts: 10277

| Bear - 2016-06-25 7:33 AM Don't get me started on Social Security. There's no earthly reason why the program should continue indefinitely. I'm waiting for a courageous politician to come out and put forth a sensible argument in favor of transitioning to a privatized system. As 1D Soon suggested, if you want to save for retirement, the best way to accomplish that is to put your money where it will work for you and grow. Allowing the fed government to confiscate it from you for your entire life won't get you there. Social Security is just as bad as a Ponzi scheme. Bank savings accounts are not money gardens, and the federal government is even worse. Politicians for decades have used criminal scare tactics to convince the unthinking that privatization is somehow dangerous. No matter where you put your money, there will always be risk. At the top of the list of lousy vehicles, in terms of investing for retirement, is social security. It's already failing. Consider this scenario. If you start contributing 12.4% of your income at age 20 to retirement, you retire at age 60, and you average an annual income of $40K per year, assuming an average annual rate of growth of 7% over those 40 years, how much would your nest egg be worth? Answer: about $1.2 Million. Don't believe me? Figure it out for yourself. Go back and look up the average rate of growth of equities over the last 100 years. If you start with the stock market crash of 1929 until present day, the average rate of growth in the market is roughly 8.5%. If you start in 1932, when the economy started to recover, the rate of growth was roughly 11%. I used a very conservative 7% figure. If I used that 11% figure, then in the above scenario, your nest egg would be worth about $3.5 million. Let's assume the less optimistic scenario of 7% - that means if you draw 5% off that nest egg to live on, your retirement income would be $60K per year for the rest of your life.....when you were used to living on much less during your working years. Your nest egg probably wouldn't change much through your retirement. That would remain as your "money tree" which could be passed on in your estate when you pass away. If you die before reaching retirement, the government can tear up that IOU, if you have no dependents. In a privatized system, it goes wherever you designate. Here's another huge, albeit less appreciated, advantage of privatization. All that money in privatized retirement would amount to an annual infusion into the economy. We're talking about hundreds and hundreds of billions of "stimulus" dollars into the private sector. That's REAL money, not borrowed money like the 2009 stimulus bill. That creates jobs. But here's another beautiful bonus, for those of you fearing that the government would be left out: all that money and those jobs generate incomes, and hence tax revenues to the fed. You want to eliminate the federal debt? Privatize social security! You want to be able to afford to provide some aid to indigents WITHOUT borrowing money or raising taxes? Privatize social security! You want to provide INCENTIVE to work? Privatize social security and it won't be long before even lazy people realize that they want in on the game. Of course maybe that is "too risky". Maybe it's too good to be true. Well, that's what our elected officials tell us anyway. After all, they are so much smarter than the rest of us........aren't they?

We would opt out if given the option | |

| | |

Location: Not Where I Want to Be | Frodo - 2016-06-25 9:35 AM Bear, when you talk about privatization, does that still stem from money the Govt took from your paycheck or a voluntary program, because most people would just simply spend the money. It would never go into savings.

Dumb should hurt, it's not the Gov. job to take care of the individual.

| |

| | |

Semper Fi

Location: North Texas | Frodo - 2016-06-25 8:35 AM

Bear, when you talk about privatization, does that still stem from money the Govt took from your paycheck or a voluntary program, because most people would just simply spend the money. It would never go into savings.

Personal responsibility is just that, PERSONAL. | |

| | |

BHW Resident Surgeon

Posts: 25352

Location: Bastrop, Texas | Frodo - 2016-06-25 8:35 AM

Bear, when you talk about privatization, does that still stem from money the Govt took from your paycheck or a voluntary program, because most people would just simply spend the money. It would never go into savings.

Everyone is afraid that the irresponsible people will just raid their private fund, and that is a legitimate concern because no reform will raise your IQ.

Here's what I'm suggesting. Keep the payment amounts into the system the same. Keep the basic rules the same.....meaning, no early withdrawals except in cases of disability. Set the earlies age at which you can withdraw at say 60. If you want to continue working, no problem...no penalty. If you don't want to draw off till a later age, no problem, let it ride. Your employer contributes 6.2% of your salary and you contribute 6.2%....basically unchanged. If you are self-employed, keep the rules the same as today. The government would have a role: to lay out a menu of investment options and to oversee that the fund is distributed according to the rules. It would provide oversight against fraud and abuse. The menu of investment options would be created by a panel of private sector advisors from across a wide spectrum.....experts in the field, so to speak. People would quickly learn some very sound investment strategies that are widely accepted for given age groups - more aggressive portfolios for the young, and more conservative as you age. Each option offered in the menu of choices would be basically like a 401K or mutual fund.....diverse. There would have to be some limits set on how much you can draw annually....say no more than 7-8%. If you choose 7% on your fund that is now valued at $1.35 million, then you will probably be living on close to a 6-figure income throughout your retirement.

I think we'd see a lot of people quickly learn about markets and investing. We'd also see a lot of people get off their asses and go to work. Also, I don't see that a separate retirement fund would be as necessary. If you want a separate fund that's fine. If you want to invest in a Roth IRA, then fine. If you want to set up a college fund for the kids, go for it. The important thing is that your " retirement security" would be yours....you own it. Government can't touch it. | |

| | |

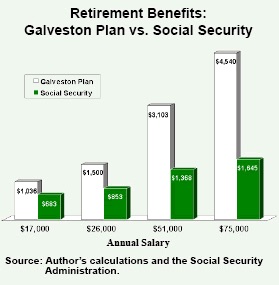

BHW Resident Surgeon

Posts: 25352

Location: Bastrop, Texas | Just in case anyone has been wondering if this plan has been put to the test, consider the Galveston county workers retirement plan. Back in 1983, a social security reform bill was passed, and one aspect of that law made it illegal for state and local governments to opt out of SS. Just before that, however, the Galveston county workers managed to slip in the door and opt out, in favor of their own privatized plan. This article compares and contrasts the payout of their plan versus SS, and the result is almost mind blowing. Keep in mind, their plan is very conservative, from an investing standpoint.

There are some differences between what I'm suggesting versus Galveston.....mine is better. Still, they get the right idea. This is from USA Today...not exactly a conservative think tank, mind you:

http://usatoday30.usatoday.com/news/opinion/2005-03-15-benefits-ref...

(image.jpg) (image.jpg)

Attachments

----------------

image.jpg (20KB - 161 downloads) image.jpg (20KB - 161 downloads)

| |

| | |

Fact Checker

Posts: 16575

Location: Displaced Iowegian | Bear - 2016-06-25 9:32 AM Just in case anyone has been wondering if this plan has been put to the test, consider the Galveston county workers retirement plan. Back in 1983, a social security reform bill was passed, and one aspect of that law made it illegal for state and local governments to opt out of SS. Just before that, however, the Galveston county workers managed to slip in the door and opt out, in favor of their own privatized plan. This article compares and contrasts the payout of their plan versus SS, and the result is almost mind blowing. Keep in mind, their plan is very conservative, from an investing standpoint. There are some differences between what I'm suggesting versus Galveston.....mine is better. Still, they get the right idea. This is from USA Today...not exactly a conservative think tank, mind you: http://usatoday30.usatoday.com/news/opinion/2005-03-15-benefits-ref... Scott and I have discussed this option at length over the past few years. I have a cousin who is enrolled in the Galveston program and seems to be very satisfied. I would have to doublecheck but I am certain that it is mandatory for them to be enrolled (just like Social Security). Edited by NJJ 2016-06-25 1:10 PM

| |

| | |

I Don't Brag

Posts: 6960

| While I somewhat agree with Scott, I cannot put any money back in the stock market. What is a person to trust for shorter term? We bought a couple of Mutual funds of different risk levels starting maybe 20 years ago?? They rose like crazy and were worth 2 1/2 times what we invested....then less than what we invested, then 1 1/2 times what we invested then less, then we got out and put our money into a guaranteed no loss annuity. Our financial planner took our annuity OUT of the stock market this last round so that we would see at least some kind of gain.

The stock market can be a great thing, but if you need your money at the bottom of a crash you are SOL. We have a little money that I would like to invest in "something" but there is nothing left. Used to have the mutual funds and a few CDs but at less than 1% (last time I checked) I am not willing to tie it up for long periods of time.

Hubby "should" be retired by now but besides getting crabby if home for long periods of time, we can't afford it. Need to keep what we have safe but sure would LIKE to put it to work for us. Right now bonds, CDs are not very viable, gold, silver etc are very volatile, the stock market just dropped like a stone thanks to Brexit (tho it would be a good time to get IN).....there seems to be no safe place to put your money anymore, especially shorter term investments. | |

| | |

Semper Fi

Location: North Texas | rodeoveteran - 2016-06-25 10:46 AM

While I somewhat agree with Scott, I cannot put any money back in the stock market. What is a person to trust for shorter term? We bought a couple of Mutual funds of different risk levels starting maybe 20 years ago?? They rose like crazy and were worth 2 1/2 times what we invested....then less than what we invested, then 1 1/2 times what we invested then less, then we got out and put our money into a guaranteed no loss annuity. Our financial planner took our annuity OUT of the stock market this last round so that we would see at least some kind of gain.

The stock market can be a great thing, but if you need your money at the bottom of a crash you are SOL. We have a little money that I would like to invest in "something" but there is nothing left. Used to have the mutual funds and a few CDs but at less than 1% (last time I checked) I am not willing to tie it up for long periods of time.

Hubby "should" be retired by now but besides getting crabby if home for long periods of time, we can't afford it. Need to keep what we have safe but sure would LIKE to put it to work for us. Right now bonds, CDs are not very viable, gold, silver etc are very volatile, the stock market just dropped like a stone thanks to Brexit (tho it would be a good time to get IN).....there seems to be no safe place to put your money anymore, especially shorter term investments.

Precious Metals i.e. Silver and gold have ALWAYS been volatile. Even more than the stock market. However, PMs will ALWAYS be worth something to someone, while stocks and bonds and yes even annuities have been known NOT to be worth they are printed on.......................... | |

| | |

BHW Resident Surgeon

Posts: 25352

Location: Bastrop, Texas | rodeoveteran - 2016-06-25 10:46 AM

While I somewhat agree with Scott, I cannot put any money back in the stock market. What is a person to trust for shorter term? We bought a couple of Mutual funds of different risk levels starting maybe 20 years ago?? They rose like crazy and were worth 2 1/2 times what we invested....then less than what we invested, then 1 1/2 times what we invested then less, then we got out and put our money into a guaranteed no loss annuity. Our financial planner took our annuity OUT of the stock market this last round so that we would see at least some kind of gain.

The stock market can be a great thing, but if you need your money at the bottom of a crash you are SOL. We have a little money that I would like to invest in "something" but there is nothing left. Used to have the mutual funds and a few CDs but at less than 1% (last time I checked) I am not willing to tie it up for long periods of time.

Hubby "should" be retired by now but besides getting crabby if home for long periods of time, we can't afford it. Need to keep what we have safe but sure would LIKE to put it to work for us. Right now bonds, CDs are not very viable, gold, silver etc are very volatile, the stock market just dropped like a stone thanks to Brexit (tho it would be a good time to get IN).....there seems to be no safe place to put your money anymore, especially shorter term investments.

You really need to do some very fundamental basic homework, Rodeoveteran. We're talking long term here. Read up on the long term gains over decades. There's always some risk no matter where you put your money. | |

| | |

"Heck's Coming With Me"

Posts: 10797

Location: Kansas | 1DSoon - 2016-06-25 8:42 AM Frodo - 2016-06-25 9:35 AM Bear, when you talk about privatization, does that still stem from money the Govt took from your paycheck or a voluntary program, because most people would just simply spend the money. It would never go into savings.

Dumb should hurt, it's not the Gov. job to take care of the individual.

Folks working their hearts out just to make a living with no extra to save don't necessarily fit in the "dumb" category.

| |

| | |

Shelter Dog Lover

Posts: 10277

| Frodo - 2016-06-25 12:03 PM 1DSoon - 2016-06-25 8:42 AM Frodo - 2016-06-25 9:35 AM Bear, when you talk about privatization, does that still stem from money the Govt took from your paycheck or a voluntary program, because most people would just simply spend the money. It would never go into savings.

Dumb should hurt, it's not the Gov. job to take care of the individual.

They would have extra to save if they were to have the SS taxes that are withheld and they would get a much better return on their money as historically proven and less waste, less corruption. | |

| | |

BHW Resident Surgeon

Posts: 25352

Location: Bastrop, Texas | How does this sound? Give people two options: privatized versus traditional SS.

Let's see how many choose traditional SS. | |

| | |

Nut Case Expert

Posts: 9305

Location: Tulsa, Ok | Frodo - 2016-06-24 1:35 PM You know how for 2016 the administration decided recipients didn't need a raise in Social Security, even though many senior citizens totally depend on it. Well, for 2017 the raise will be.. (drumroll).. two-tenths of one percent, or about $3 per recipient. Why bother? The real kick in the teeth is when I see illegals interviewed on TV counting their numerous blessings from U.S. taxpayers and including Social Security in the mix.

You do realize that the "administration" didn't just arbitrarily decide on the amount of the increase. The law governing the increase is tied to the government measure of inflation. If congress as a whole (both republicans and democrats) gave a rats ass they could address the problems of social security and medicare. But bottom line ALL of them are more concerned about their own posturing and bickering to really care about seniors. | |

| | |

Nicknameless

Posts: 4565

Location: I can see the end of the world from here! | Bear - 2016-06-25 6:33 AM Don't get me started on Social Security. There's no earthly reason why the program should continue indefinitely. I'm waiting for a courageous politician to come out and put forth a sensible argument in favor of transitioning to a privatized system. As 1D Soon suggested, if you want to save for retirement, the best way to accomplish that is to put your money where it will work for you and grow. Allowing the fed government to confiscate it from you for your entire life won't get you there. Social Security is just as bad as a Ponzi scheme. Bank savings accounts are not money gardens, and the federal government is even worse. Politicians for decades have used criminal scare tactics to convince the unthinking that privatization is somehow dangerous. No matter where you put your money, there will always be risk. At the top of the list of lousy vehicles, in terms of investing for retirement, is social security. It's already failing. Consider this scenario. If you start contributing 12.4% of your income at age 20 to retirement, you retire at age 60, and you average an annual income of $40K per year, assuming an average annual rate of growth of 7% over those 40 years, how much would your nest egg be worth? Answer: about $1.2 Million. Don't believe me? Figure it out for yourself. Go back and look up the average rate of growth of equities over the last 100 years. If you start with the stock market crash of 1929 until present day, the average rate of growth in the market is roughly 8.5%. If you start in 1932, when the economy started to recover, the rate of growth was roughly 11%. I used a very conservative 7% figure. If I used that 11% figure, then in the above scenario, your nest egg would be worth about $3.5 million. Let's assume the less optimistic scenario of 7% - that means if you draw 5% off that nest egg to live on, your retirement income would be $60K per year for the rest of your life.....when you were used to living on much less during your working years. Your nest egg probably wouldn't change much through your retirement. That would remain as your "money tree" which could be passed on in your estate when you pass away. If you die before reaching retirement, the government can tear up that IOU, if you have no dependents. In a privatized system, it goes wherever you designate. Here's another huge, albeit less appreciated, advantage of privatization. All that money in privatized retirement would amount to an annual infusion into the economy. We're talking about hundreds and hundreds of billions of "stimulus" dollars into the private sector. That's REAL money, not borrowed money like the 2009 stimulus bill. That creates jobs. But here's another beautiful bonus, for those of you fearing that the government would be left out: all that money and those jobs generate incomes, and hence tax revenues to the fed. You want to eliminate the federal debt? Privatize social security! You want to be able to afford to provide some aid to indigents WITHOUT borrowing money or raising taxes? Privatize social security! You want to provide INCENTIVE to work? Privatize social security and it won't be long before even lazy people realize that they want in on the game. Of course maybe that is "too risky". Maybe it's too good to be true. Well, that's what our elected officials tell us anyway. After all, they are so much smarter than the rest of us........aren't they?

I hope you don't mind (if you do? Too bad! lol) I c/p'd this to Mike Lee's fb...smile on!

| |

| | |

I Don't Brag

Posts: 6960

| Bear - 2016-06-25 11:42 AM

rodeoveteran - 2016-06-25 10:46 AM

While I somewhat agree with Scott, I cannot put any money back in the stock market. What is a person to trust for shorter term? We bought a couple of Mutual funds of different risk levels starting maybe 20 years ago?? They rose like crazy and were worth 2 1/2 times what we invested....then less than what we invested, then 1 1/2 times what we invested then less, then we got out and put our money into a guaranteed no loss annuity. Our financial planner took our annuity OUT of the stock market this last round so that we would see at least some kind of gain.

The stock market can be a great thing, but if you need your money at the bottom of a crash you are SOL. We have a little money that I would like to invest in "something" but there is nothing left. Used to have the mutual funds and a few CDs but at less than 1% (last time I checked) I am not willing to tie it up for long periods of time.

Hubby "should" be retired by now but besides getting crabby if home for long periods of time, we can't afford it. Need to keep what we have safe but sure would LIKE to put it to work for us. Right now bonds, CDs are not very viable, gold, silver etc are very volatile, the stock market just dropped like a stone thanks to Brexit (tho it would be a good time to get IN).....there seems to be no safe place to put your money anymore, especially shorter term investments.

You really need to do some very fundamental basic homework, Rodeoveteran. We're talking long term here. Read up on the long term gains over decades. There's always some risk no matter where you put your money.

Did you not see where I said that I somewhat greed with you? I am not entirely stupid or unaware of the stock market's trends. But if you are the unfortunate soul who needs their money at the bottom of a bear market, you are SOL. Just wasn't raised to be a big risk taker when it comes to money. lol

I have had financial advisors show me all the charts and those dips just scare the pants off me, especially short term, which is what I SPECIFICALLY questioned about. We don't have decades to ride out the market. And all of those trends are assuming that you invest in the correct stocks, which they showed years ago that a literal monkey could choose as successfully or better than a human, studied and educated in the market.

Now if my truck driver hubby applied himself to Wall Street like he has the trucking industry, I would bet on him. He has a knack for seeing trends, laws and other things that affect his industry that have kept us from losing money when others lost their butts. I think if he had a will and passion to apply that to the stock market he could be a great investor and manager of our funds.

Since I am waiting for hyper inflation and a true Depression (I have to laugh when the last little recession we have not yet emerged from) to hit in the near future and I want my funds no where near the market (until it bottoms out, then I might dip my toes back in the water). The market has been held up artificially for at least this POTUS' term by the printing of money which is then funneled in to the stock market. There will be a BIG price to pay for that. | |

| | |

"Heck's Coming With Me"

Posts: 10797

Location: Kansas | rodeoveteran - 2016-06-26 9:50 PM Bear - 2016-06-25 11:42 AM rodeoveteran - 2016-06-25 10:46 AM While I somewhat agree with Scott, I cannot put any money back in the stock market. What is a person to trust for shorter term? We bought a couple of Mutual funds of different risk levels starting maybe 20 years ago?? They rose like crazy and were worth 2 1/2 times what we invested....then less than what we invested, then 1 1/2 times what we invested then less, then we got out and put our money into a guaranteed no loss annuity. Our financial planner took our annuity OUT of the stock market this last round so that we would see at least some kind of gain. The stock market can be a great thing, but if you need your money at the bottom of a crash you are SOL. We have a little money that I would like to invest in "something" but there is nothing left. Used to have the mutual funds and a few CDs but at less than 1% (last time I checked) I am not willing to tie it up for long periods of time. Hubby "should" be retired by now but besides getting crabby if home for long periods of time, we can't afford it. Need to keep what we have safe but sure would LIKE to put it to work for us. Right now bonds, CDs are not very viable, gold, silver etc are very volatile, the stock market just dropped like a stone thanks to Brexit (tho it would be a good time to get IN).....there seems to be no safe place to put your money anymore, especially shorter term investments. You really need to do some very fundamental basic homework, Rodeoveteran. We're talking long term here. Read up on the long term gains over decades. There's always some risk no matter where you put your money. Did you not see where I said that I somewhat greed with you? I am not entirely stupid or unaware of the stock market's trends. But if you are the unfortunate soul who needs their money at the bottom of a bear market, you are SOL. Just wasn't raised to be a big risk taker when it comes to money. lol I have had financial advisors show me all the charts and those dips just scare the pants off me, especially short term, which is what I SPECIFICALLY questioned about. We don't have decades to ride out the market. And all of those trends are assuming that you invest in the correct stocks, which they showed years ago that a literal monkey could choose as successfully or better than a human, studied and educated in the market. Now if my truck driver hubby applied himself to Wall Street like he has the trucking industry, I would bet on him. He has a knack for seeing trends, laws and other things that affect his industry that have kept us from losing money when others lost their butts. I think if he had a will and passion to apply that to the stock market he could be a great investor and manager of our funds. Since I am waiting for hyper inflation and a true Depression (I have to laugh when the last little recession we have not yet emerged from ) to hit in the near future and I want my funds no where near the market (until it bottoms out, then I might dip my toes back in the water ). The market has been held up artificially for at least this POTUS' term by the printing of money which is then funneled in to the stock market. There will be a BIG price to pay for that.

Edited by Frodo 2016-06-27 11:29 AM

| |

| |

|